Carbon trading dogma: Theoretical assumptions and practical implications of global carbon markets

Keywords

- abstract

This article argues that the analysis of the commodities exchanged on global carbon markets can help us grasp the current relationship between economic categories and environmental issues. In the article, global carbon markets are historically contextualized, analytically described and politically articulated against the background of two hypotheses: (1) that the process of progressive marketization of climate change occurs in connection with the emergence of a new modality of value production (which can be generically defined as ‘cognitive capitalism’); and (2) that the governance of contemporary circuits of valorization tends to be located within the financial sphere and poses a constitutive and ongoing uncertainty/instability as a necessary condition for their reproduction. Subsequently, these hypotheses are tested with specific reference to the ‘Clean Development Mechanism’ as established by the Kyoto Protocol. In particular, the analysis will focus on the carbon commodities known as ‘Certified Emission Reductions’, which reveal an unprecedented relationship between use-value and exchange-value. I contend that the use-value of carbon commodities is not defined by an intrinsic ecological dimension; rather, it is produced under the exclusive condition of accepting the redeeming character of the market as fundamentally shaped by the formal principle of economic competition. The paper aims to demonstrate how the value produced in global carbon markets rests exclusively on the social actors’ arbitrary acceptance of the ‘carbon trading dogma’, namely an extremely entrenched – albeit empirically unprovable – political belief that climate change, although a market failure, can be viably solved only by further marketization.

Introduction*

The present article builds on the hypothesis that the green economy is a capitalist attempt to overcome recent socio-ecological crises by incorporating the environmental limit as a new terrain for accumulation and valorization. In other words, I propose a historical account of the relationship between nature and value: whereas liberal governmentality conceived of the environment as an internal limit – i.e. a moment of mediation – of the process of valorization, starting in the 1970s neoliberal governmentality has perceived nature as an immediate, direct element of value-creation (Leonardi, 2012).

Against this background, two further research questions become important:

i) Under what conditions could carbon markets actually work? In other words, what criteria define the positive or negative functioning of such devices?

ii) Can the inclusion of climate change within market mechanisms have, or has it had, an incentive-effect with regard to the abatement of greenhouse gases (GHGs) emissions? In other words, can an efficiency-based cost-benefit analysis yield realistic solutions to the dramatic implications of global warming?

In this paper, I attempt to answer these questions. To do so, I first briefly discuss the historical trajectory of carbon trading, both theoretically and in terms of practical implementation. Second, I propose a definition of carbon trading dogma specifying its essential elements and situating it against the background of two tendencies in contemporary capitalist development: the progressive cognitization of labour and the pervasive financialization of life. Third, I advance the hypothesis that the use-value of the specific commodity called ‘carbon’ should be conceived of as information. Fourth, I turn attention to carbon credits or carbon offsets, in particular the Certified Emissions Reductions (CERs): analysis of the CER regime allows me to investigate how the carbon trading dogma penetrates the subjective practices of those social actors who politically engage global warming on a regular basis – be they carbon traders, climate justice activists or ‘green’ agencies’ officials. The paper concludes by pointing out possible lines of further research and political action.

Brief history and critique of carbon trading

To get a rough and ready idea of the evolution of carbon markets, it may be useful to start with some World Bank statistics (2007; 2008; 2009; 2010b; 2011; 2012; 2014). In terms of market value, carbon trading in its entirety – compliance and voluntary markets, as well as primary and secondary markets[1] – was worth approximately US $10 billion in 2005, and triple that in 2006. In 2007, the volume of carbon trading reached $63 billion, doubling again in 2008. Despite the global economic crisis, carbon trading grew again in 2009 by 8%, with a total amount of trade volume worth US $143 billion. In 2010, however, the effects of the financial crisis were also felt in the realm of carbon economy, causing it to slightly drop to US $142 billion. Surprisingly enough, notwithstanding the deepening of the economic downturn, 2011 saw a robust increase in transaction volumes (establishing a record high 10.3 billions tCO2e)[2] with an aggregate value of US $176 billion. The year 2012 was a troubling one for carbon markets, due mainly to a reduced confidence in them by private and public sectors alike: the failure of the COP 17 climate negotiations in Durban revealed an international scenario in which the second commitment period (2012-2020) of the Kyoto Protocol (KP2) covered only 12% of global GHGs emissions.[3] Subsequently, Kyoto credit prices reached their historic lows in 2013 and 2014, with Certified Emission Reductions (CERs) worth just US $0.51 (€0.37). Despite this decrease, the World Bank remained confident that ‘a consensual and robust international solution could revive private sector confidence to invest in carbon markets’ (World Bank, 2014: 14). Many policy makers hope such solution has been found at the COP 21, but a positive economic performance of the Paris Agreement cannot be taken for granted (Moreno, Fuchs and Speich Chassé, 2016).

In general terms, although prices have constantly fluctuated, the market trend continued to grow at different paces until 2012. Given the current absence of policy alternatives, political expectations remain overly optimistic, and carbon trading is expected to expand. Drawing on three different estimates, Robert Fletcher reports that aggregate carbon trading is predicted to reach a value of US $2-3 trillion by 2020 and US $10 trillion around 2030 (Fletcher, 2012).

Regardless of future trends, however, carbon markets catalyse a significant share of economic activity and policy imagination. This is rather surprising, given their relatively recent implementation. In fact, although the direct proportionality between the levels of carbon dioxide (CO2) in the atmosphere and the surface temperature of the earth was discovered already in 1896, when Svante Arrhenius, drawing on previous speculations by other scientists, gave full account of the greenhouse effect, the emergence of a collective awareness about the damaging potential of global warming arose only in the 1980s (Chakrabarty, 2009). In 1992, the United Nations Conference on Environment and Development (held in Rio de Janeiro) – also known as the Earth Summit – released an international environmental treaty known as the United Nations Framework Convention on Climate Change (UNFCCC), the objective of which was to stabilise GHG concentration in the atmosphere at a level that would prevent dangerous human-induced interference with the climatic system. Since the treaty entered into force in 1994, the signatory states have been meeting annually in Conferences of the Parties (COP) to assess progress in the field of global climate policy.

Of particular importance was COP 3, held in Kyoto in 1997, during which the parties agreed to sign a Protocol to the UNFCCC, known as the Kyoto Protocol (KP). As the first legally binding agreement on climate change, the KP provides that the 37 Annex I countries (or the so-called developed nations) commit themselves to a reduction of six GHGs (5.2% on average in the 2008-2012 period, using 1990 as a baseline year), and all members (including Annex II countries, i.e. the so-called developing nations) give general commitments. The KP is intended to achieve emissions reductions through a variety of approaches: promoting international cooperation and substantial technology transfers; intervening at the source by means of energy saving and energy efficiency strategies; and accounting for emissions sequestration performed by natural carbon sinks. However, its crucial innovation is carbon trading, i.e., allocating and exchanging carbon commodities viewed as the most efficient solution to the climate crisis (Iacomelli, 2005). In fact, under the powerful political pressure exercised by the US delegation – led by then Vice-President Al Gore – the parties agreed to structure both the design and the implementation of the KP around three market-led approaches, termed flexibility mechanisms: i) Emissions Trading (ET), namely a cap-and-trade system in which governmental authorities set emission caps and private companies exchange permits and credits; ii) Joint Implementation (JI), a regulative system for exchanges amongst Annex I countries; and iii) Clean Development Mechanism (CDM), the function of which is to indirectly include Annex II countries in global carbon markets.[4] The fundamental economic rationale offered for such mechanisms is that trading emissions permits and credits on dedicated markets would act simultaneously to reduce the aggregate cost of meeting the targets, foster sustainable development in non-industrialized countries and create profitable opportunities for green business.

These objectives, however, never materialized. There is an abundant body of literature on the flaws of the KP (both internal and external to its own logic).[5] For example, Gupta et al. (2007), in their detailed review of climate change policy literature, found that no credible assessments of the KP contended that it had had, or will have, any relevant impact on solving the global warming crisis. Even the World Bank (2010a) reported that the KP has had only a slight effect on curbing emissions increase. Moreover, it has been noted that cap-and-trade systems – amongst which the most relevant is the EU ETS (European Union Emissions Trading System) have proved slightly resilient only because of grandfathering, i.e. the gratuitous and excessive allocation of European Union Allowances (EUA) (AAVV, 2013). Furthermore, recurrent fraud seems to be plaguing the design and implementation of CDM projects: accountability is an obvious difficulty, and corruption has been widespread (Lohmann, 2011a). No alternatives to existing carbon trading schemes have been envisaged and implemented so far: the carbon trading ‘solution’ seems to have exhausted the UNFCCC policy imagination. Even the COP 21 Paris Agreement, elaborated in 2015, is more likely to expand rather than decommission carbon markets (Marcu, 2016).

What is the carbon trading dogma?

To explain this insistence on carbon trading as an exclusive policy option, it may be useful to refer to the two registers of the climate change debate. Allow me to elaborate by way of a recent example. In his opening address to the 2014 Climate Summit held in New York,[6] UN Secretary-General Ban Ki-moon argued that decisive climate action cannot be further delayed:

No one is immune from climate change, not even this UN HQ, which were flooded during super-storm Sandy. We must invest in climate resilient societies that protect all, especially the most vulnerable. I ask all governments to commit to a meaningful climate agreement in Paris in 2015. (reported in Vaughan and Mathiesen, 2014)

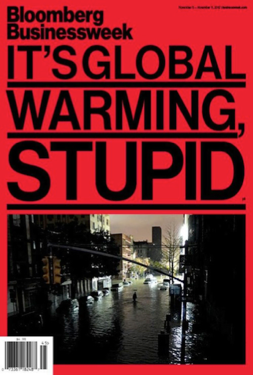

His reference to Sandy – which killed more than 100 people in the Caribbean and the east coast of the US in October 2012 – is especially interesting given the particular way American media covered it. Sandy hit the US just a few days before the 2012 presidential elections. In keeping with the political mood of the campaign (Obama vs. Romney) which was astoundingly silent about global warming (the first time since 1984 that climate change was not mentioned in the electoral debates), the mainstream media refused to link Sandy – and more generally the increased frequency and intensity of extreme weather events – to anthropogenic climate change.[7] In this context, the November 1st issue of Bloomberg Businessweek was a welcome exception, being an unlikely supporter, albeit before the fact, of UN Secretary-General Ban Ki-moon’s call to action.

Figure 1: Cover of Bloomberg Businessweek.

Its cover story, entitled ‘It’s Global Warming, Stupid’ is instructive for the way in which the climate change debate has evolved. Journalist Paul Barrett initially discusses a series of scientific data which suggest a direct correlation between human activity and climate modifications. This is the first register of the global warming debate: it concerns mainly the issue of whether or not the root cause of climatic imbalances is anthropogenic. My reflection here does not address this problematic: although climate science should not be regarded as the guardian of an eternal and indisputable truth, scientific as well as experiential evidence supporting the human-induced nature of climate change is today so abundant that controversies refer more to its specific configurations than to its actual existence (Oreskes and Conway, 2010).

More interestingly from my perspective, Barrett’s article also introduces the second register of the global warming debate, namely its possible solutions. And it is here that what I call the carbon trading dogma comes into full view. This dogma is an extremely entrenched – albeit empirically unprovable – political belief that climate change, although a market failure (the environment was never properly accounted for by the price-system), can be viably solved only by a wave of further marketization. Barrett articulates the shift from the first to the second register by declaring:

If all that [lists of scientific data] doesn’t impress, forget the scientists ostensibly devoted to advancing knowledge and saving lives. Listen instead to corporate insurers committed to compiling statistics for profit. (Barrett, 2012: 7)

Barrett then cites a report issued by the financial re-insurance company Munich: Re, according to which climate change is causing a rising number of natural catastrophes, especially in North America. His conclusion is peremptory: if financial analysts believe climate change is occurring, then there is no point in questioning it anymore.

This passage entails a curious reversal of modern rationality, ostensibly centred on the sharp distinction between facts (science) and values (politics and/or ethics). The financial colonization of climate change as a global political issue, in fact, relies on a paradoxical inversion of modern categories: ‘You don’t trust science? Fine. But you must believe in markets!’. In other words, in Barrett’s argument, the market functions as a site of veridiction, as Michel Foucault suggested in his biopolitical lectures from the late 1970s (Foucault, 2007; 2008; Dardot and Laval, 2014). In the context of potentially catastrophic global warming, such a market-based regime of truth gives rise to a dogmatic equation – as discursively indisputable as it is empirically unprovable – that, elaborating on recent work by Larry Lohmann (2011c), might be defined as follows:

climatic stability = reductions in CO2 emissions = carbon trading = sustainable economic growth

The strength of this dogma is demonstrated not only by climate policy makers’ insistence on the utility of carbon markets, despite their irrelevant – if not negative – ecological impacts, but also by the increasing difficulties encountered by market actors in justifying the narratives of green economy and sustainable growth (Descheneau and Paterson, 2010). The circular logic of the carbon trading dogma makes any alternative unthinkable: like any religious dogma, the confirmation of its truth claims is already contained in its fundamental assumption: since there is no effective politics outside of the market, global warming is solvable only in so far as it is possible to make a profit out of it. ‘Climate stability equals surplus value production’ is treated as self-evident truth.

The circular nature of the carbon trading dogma and its extreme entrenchment, however, are not sufficient to properly grasp the historical novelty it represents. In fact, its evolution needs to be situated in the context of the two elements that characterise the current, neoliberal tendency of capitalist development: the emergence of new forms of valorization and exploitation, which can be defined as cognitive capitalism; and the rise of financialization as the most pervasive governmental dispositif.[8] With regard to cognitive capitalism, we observe the appearance of the general intellect as a novel configuration of the notion of real abstraction (Virno, 2004), as well as the unprecedented role played by knowledge in the realm of productive activity.[9] Knowledge today is not simply a precondition for production. It is at the very centre of the production process (Lucarelli and Vercellone, 2013). It is, in other terms, the fundamental productive factor, such that the economy can be said to rely on the production of knowledge by means of knowledge. This is a circular process whereby the output constantly regenerates the input through relatively cheap innovation based on seemingly endless reproducibility. Such a formulation implies an understanding of the general intellect as the organising principle of contemporary production.[10]

By transposing such reflections on the global warming terrain, it is possible to realize how the very visibility of climate change relies on complex, contested and always re-negotiable knowledge infrastructures. As historian Paul Edwards argued:

Instead of thinking about knowledge as pure facts, theories, and ideas – mental things carried around in people’s heads, or written down in textbooks – an infrastructure perspective views knowledge as an enduring, widely shared socio-technical system. Knowledge infrastructures comprise robust networks of people, artefacts, and institutions that generate, share, and maintain specific knowledge about the human and natural worlds. (2010: 17)

In this sense, to experience a global warming event as such presupposes the infrastructural support of climate science. In other words, linking a weather-related event – no matter how extreme – to climate change requires a massive mobilization of the general intellect in its diverse forms (various knowledge-factories such as universities, think-tanks, activists’ counter-narratives, etc.). Obviously, this dependence on knowledge does not make climate change any less concrete or material, both in the individuation of its multiple causes and in the destructiveness of its heterogeneous effects.

As for the financialization aspect of the contemporary capitalistic tendency, I propose to approach financialization as a governmental dispositif and to uncover its affinity with carbon trading, as a particular yet dominant form of climate policy. By ‘financialization’ I mean a set of practices through which companies, institutions and individuals become completely embedded in financial transactions. The outcome of this process is an unprecedented dependence on unstable markets and volatile money for everything from food supplies to services, from education to income. Granted, finance has been a feature of the capitalist mode of production since its beginnings; nonetheless, the current configuration of finance is qualitatively and quantitatively unique, unprecedented in its extent, with a massive proliferation of sophisticated and opaque financial tools such as derivatives, Credit Default Swaps, Collateralized Debt Obligation. These technologies represent an immensely complicated and coordinated attempt to make profit out of the financial colonization of every aspect of social life.

As Christian Marazzi wrote:

Financialization is not an unproductive/parasitic deviation of growing quotas of surplus-value and collective savings, but rather the form of capital accumulation symmetrical with new processes of value production. Today’s financial crisis should then be interpreted as a block of capital accumulation rather than an implosive result of a process lacking capital accumulation. (2011: 48)

Two consequences of this new role of finance should be emphasized:

i) Its endless expansion leads eventually to abstract self-reflexivity (Marazzi himself, by referring to the dot-com bubble of 2000, talks of a crisis of overproduction of self-referentiality);

ii) A new form of accumulation requires an institutional counterpart. In fact, financialization fundamentally transformed managerial practices in at least three central areas: in business strategy, it privileged the logic of shareholder activism; in wage relations, it internalized workers by turning them into powerless micro-shareholders;[11] in everyday life activities, it colonized people’s lives by capturing them in the debt process (from student loans to pension funds). In general, we are witnessing the deployment of a veritable mode of governing through instability, an expansion of financial reason to society as a whole (Lucarelli, 2010). Again in Marazzi’s words:

The very concept of accumulation of capital was transformed. It no longer consists, as in the Fordist period, of investment in constant and variable capital (wage), but rather of investment in apparatuses of producing and capturing value created outside directly productive processes. (2011: 54)

My contention is that such an expansion is clearly visible in the field of climate governance, with carbon markets functioning as ‘apparatuses of producing and capturing value created outside directly productive processes.’ Two aspects are of peculiar relevance to the economy of the present argument: first, the pervasiveness of financial systems has not spared climatic alterations; in fact, carbon trading mobilises complex hybrid instruments (simultaneously financial and environmental), such as weather-derivatives and CAT bonds (catastrophe bonds);[12] and, second, carbon markets share with the financial sphere a constitutive attitude towards instability: the complexity of procedures for producing, measuring, and exchanging carbon commodities closely resembles the opaque trade in derivatives. What needs to be emphasized is that in both cases, such instability does not result from the imperfect application of otherwise correct protocols. Rather, it is a necessary condition for the production of these particular commodities.

Information as use-value of carbon commodities

The double perspective provided by cognitive capitalism and financial governmentality is useful in addressing the following question: Why are policy makers so reliant on carbon markets when empirical evidence suggests that they do not work? In fact, their peculiar failure can be expressed through a curious paradox: from an ecological point of view – the environmental degradation that carbon trading is supposed to solve (through the reduction of GHGs emissions to slow down global warming) – it is fair to say that carbon markets are useless when not nefarious. Quite simply, they do not achieve the expected results or, worse, actually prevent such achievements from occurring.[13] From an economic perspective, however, such markets represent a gold mine for financial traders (as well as heavy polluting companies). These markets function through a logic that is similar to that described by Foucault for the pre-modern French prison system: with Lohmann’s brilliant paraphrase, it is possible to conclude that carbon trading ‘has always been offered as its own remedy: the reactivation of its techniques as the only means of overcoming its perpetual failure [...] the supposed failure is part of its functioning’ (Foucault quoted in Lohmann, 2011b: 102). Here again, we see how uncertainty and instability act as governmental tools to manage socio-environmental dynamics. There seems to be a manifest disconnect between the environmental goal and the economic means of carbon trading. In fact, although no ecological improvement has been made, a huge amount of value has been created and then transferred to fossil fuel-intensive companies through the production of what can be called climate rent.[14] As Lohmann aptly points out: ‘The fact that governments are both suppliers and regulators of emissions commodities has encouraged rampant rent-seeking and complicated allocation schemes that profit, rather than penalise, heavy polluters’ (quoted in Reyes, 2011: 6). It is probably more accurate, therefore, as well as more empowering, to say that carbon trading is environmentally irrelevant, rather than claiming that it simply does not work. Carbon trading has had a significant economic impact – though this has fluctuated over time (frequent carbon price collapses have repeatedly undermined the markets’ credibility even on their own terms). This friction between environmental irrelevance and rent production has led to the entrenchment of the carbon trading dogma. Hence, although the ecological inconsistency of carbon markets has been empirically demonstrated on innumerable occasions, the assumption of a harmonic compatibility between climate stability and sustainable growth keeps orienting policymakers as well as market actors.

Why are carbon markets characterized by this sort of productive failure? A first hypothesis is that the marketization of global warming is a pure and simple ideological operation. According to Patrick Bond, for example, the green rhetoric based on the undemonstrable affinity between environmental preservation and capitalist valorization is actually aimed at sustaining the oil industry and co-opting social oppositions (Bond, 2012b). In other words, carbon trading is nothing but a smokescreen that conceals the logical and historical impossibility of a consonance between a healthy environment and the capitalist mode of production. A ‘lucrative scam’, in Naomi Klein’s terms (2014: 8). Although such an argument has merit, it is also true that capitalism has repeatedly demonstrated, in the course of its history, a profound adaptability. Elaborating on this malleable feature, Actor Network Theory scholars such as Michel Callon approach carbon markets as social experiments susceptible to improvements (Callon, 2009). Moreover, it is not clear what a full rejection of carbon markets would amount to: an ambiguous nostalgia for a putative Golden Age can often be felt in the discourses of climate justice movements. At times, the shadow of Neo-Primitivism seems to haunt the critics of carbon trading, and while primitivist politics would surely imply a major reduction of GHGs emissions, it is debatable that it could drive desirable social change.

For these reasons, I propose to frame the critique of carbon trading by focussing on the particular nature of the commodities that are exchanged in it. As research-activists Tamra Gilbertson and Oscar Reyes have argued:

The commodity traded as ‘carbon’ does not actually exist outside the numbers flashed up on trading schemes or the registries held by administrators […] This makes putting a price on carbon largely an arbitrary exercise. (2009: 12-13)

Analogously, the Transnational Institute’s Carbon Trade Watch remarks: ‘These failings [of carbon trading] are not caused by teething problems, but are symptomatic of the extreme difficulties of assessing the value of “carbon”, a commodity which bears little relation to any single real world object’ (quoted in Bond and Sharife, 2012: 15). In a similar vein, Descheneau and Paterson locate the difference between Carbon EXPO and other momentous market fairs in the irreducible non-comparability between the products being sold:

While new products such as the iPad are clearly hyped enormously, the hype has some relationship to the (purported) use-value of the object. By contrast, the products in the carbon market have no use-value. The tonne of carbon refers to a tangible unit of measure, but demands for the right to emit it arise purely out of government regulatory activity. The tonne of carbon has thus to be abstracted to something more tangible for market actors, i.e. financial or monetary products. Thus, what is being sold is not the tonne per se but rather the financial or discursive representations of it. (Descheneau and Paterson, 2011: 667-668; my emphasis)

The big picture that emerges from these insights is a rather confused one: on what basis can we make sense of a use-value that would be, by turns, composed of numerical calculations, defined by its absence, and resembling an unreal world object? To answer this question, we might recall Marx’s view of the relationship between use-value and exchange-value within the capitalist mode of production. According to Marx, capitalism can be adequately understood as a machine of abstraction. The process of valorization upon which it rests is first and foremost defined by its indifference toward the concrete qualities that, in other modes of wealth production, are used to define objects (or products, or ‘things’). In the Grundrisse, Marx refers to the opposition between the ‘natural distinctness’ of use-values and the ‘economic equivalence’ of exchange-value (Marx, 1993: 141). Early capitalist real abstractions (labour, money, etc.) were grounded on a valorising detachment from the kind of usefulness that was presupposed as naturally existing outside the commodity-form. This is why use-value, in Marx, does not receive extensive elaboration: it is supposed to be the natural, pre-existing modality of satisfying equally pre-existing social needs. This is, in the last instance, what a commodity is, i.e. a ‘good’ kept in a bundle of social relations such that its value does not reside in its material usefulness but in its capability to be exchanged for money: ‘The existence of the things qua commodities, and the value-relation between the products of labour which stamps them as commodities, have absolutely no connection with their physical properties and with the material relations arising therefrom’ (Marx, 1990: 83). In the context of carbon trading, however, such a presupposition no longer completely holds true: what kind of natural, external, pre-existing need would a tonne of carbon dioxide equivalent (tCO2e) satisfy? None, I would argue. Should we then conclude, with Descheneau and Paterson, that carbon commodities have no use-value? I would argue that this is not the proper way to frame the issue: arguing for the non-existence of carbon use-value would expel any intentionality whatsoever from the valorization process. How, in fact, would capital self-valorise without the gap between a social need and the commodity which is supposed to satisfy it? In other words, the disappearance of use-value implies a too severe diagnostic: the economic system as a whole would suffer from Obsessive Compulsive Disorder.

A viable alternative consists in conceiving of carbon commodities’ use-value as information. As such, this kind of use-value transcends (while still maintaining a relationship with it) the interplay between ‘natural distinctness’ and ‘economic equivalence’ as reciprocally indifferent. It is very difficult to isolate what is natural from what is economic in them[15]. In fact, what makes carbon information useful? To answer this question, we need to trace the production of relevant carbon information back to the carbon trading dogma that links climate stability to sustainable growth via financial governing through instability. Against this background, carbon commodities’ use-value is simply the dogmatic assumption that climate markets will make the transition to a low carbon society in a manner that would be more cost-effective than any other political strategy. If this is true, if carbon information possesses a use-value only insofar as it conforms to the carbon trading dogma, then it is impossible to view it as ‘naturally distinct’ from its exchange-value. Carbon commodities make it impossible to distinguish a natural need, at the beginning of the economic process, and its artificial satisfaction, at the end of the process. The commodity-form usually establishes its indifference between use-value and exchange-value precisely on the basis of this distinction. To the contrary, the regime of truth that affirms the manageability of the climate crisis only by means of competitive financial markets ends up establishing the paradoxical self-indifference of carbon commodities. It concerns a social use-value which originates directly from capitalist circuits of valorization and an equally social exchange-value, the status of which is irremediably split: on the one hand, to perform its monetary function, it must be indifferent to its use-value; on the other hand, however, it receives its very meaning by the same regime of truth that created its use-value, making the two aspects indissociable. In addition to the extensive tension between ‘natural distinctness’ and ‘economic equivalence’ (still active, albeit not thoroughgoing: after all, a tonne of carbon dioxide does exist beyond carbon information), there occurs an intensive division within the field of ‘economic equivalence’ in a way that perfectly mirrors the self-reflexivity typical of finance as a mode of capital accumulation. Whereas the extensive dimension of the commodity-form can be referred to as first order abstraction, in which the general equivalent acts as a counterpart to a putative external nature, the intensive dimension of the commodity-form should be labelled as a second order abstraction, since money becomes the unsurpassable limit, as well as the original seal, of the knowledge-based process by means of which new use-values are created to conform to neoliberal capital’s needs.

From the perspective of carbon trading, therefore, the most significant process of valorization takes place in the internal stratification of carbon as a second order abstraction: in order for value to be created, various sources of collective knowledge must be put to work so that a permanent state of uncertainty allows climate markets to re-instate their sovereignty over the management of global warming even in the face of their blatant environmental failure. As Jerome Whitington compellingly put it:

‘Carbon’ is not a physical commodity even if it includes certain physical parameters. ‘It’ is an assemblage of agreements, conventional practices, durable artifacts and rules held among people who operate in very different contexts around the world […] The clearest demonstration that carbon dioxide is not a physical commodity is that lots of different GHGs are traded as equivalent based on units of ‘carbon dioxide equivalence’ (CO2e), expressed in tons, which is actually an equilibration of the gases’ effect on the warming of the atmosphere. It is the gases’ warming effect that has value, whether operationalized as a permit or a reduction. (Whitington, 2012: 118-119; my emphasis)

This quote illustrates the character of carbon commodities as second order abstractions. Within them, in fact, the distinction between ‘natural distinctness’ and ‘economic equivalence’ tends to blur, and a decisive element of their exchange-value resides in the ex ante creation of capital-based use-values. The underlying tension between the moment of informational heterogeneity (differentiated knowledge-sources organized by the general intellect) and the moment of monetary equivalence (situated both at the beginning of the process – capital’s need to self-valorise – and at the end of the process – realization through verification) is at the very heart of the mode of governing through financial instability. Let us note that the problem raised here is entirely political: the argument according to which carbon trading can be improved by means of creating more and better information hides the bare fact that knowledge production is today the very battlefield upon which the antagonism between capital and labour (in the form of the general intellect) takes place.

How to make a CER: In the lab of carbon commodities

In order to better understand the notion of carbon commodities as second order abstractions, I shall now turn my attention to the production of Certified Emission Reductions (CERs), which are the credit units, or offsets, that are exchanged within the framework of the Clean Development Mechanism. In a nutshell, Annex I countries are allowed to meet part of their emission reduction commitments by buying CERs from CDM emission reduction projects in Annex II countries. In other words, the CDM allows the global North to invest in emission reductions through CERs where it is cheapest, which is usually in the global South.

As already discussed, the CDM is structured around the positive value attributed to economic flexibility and the assumption that cost-effectiveness is the one-best-way to enact a transition to a low-carbon society. As corollaries to these two conceptual and evaluative pillars, there are three crucial assumptions that we can define as intermediate apparatuses of the carbon trading dogma:

a) Emission reductions occur on a plane of perfect commensurability, which means that it does not matter where, when and how they materialise: a tCO2e is independent from its own spatio-temporal coordinates.

b) As a consequence, it is more cost-effective to save emissions not at source, which is to say where they are actually produced, but elsewhere (or: on the plane of commensurability) through technology transfers or various investments in renewable energy.

c) In order for the process of decarbonization to be effective, it is necessary that developing economies from the global South be included in it.

With the partial exception of the third assumption – whose geopolitical nature is unmistakable[16] – the truth-value of this entire structure strictly depends on the unconditional adherence to the dogmatic equation we uncovered above. In fact, there is no empirical proof of market superiority concerning cost-efficiency, nor is there evidence for the ineffectiveness of reductions at source, or the validity of the emissions’ perfect commensurability. In essence, what provides the CDM categorical framework with its consistency is the putative impossibility to think climate change policies outside of their market-based dimension. The performative rhetoric of economic competition works as a pre-analytic vision that shapes global warming: outside of their translation into the empty and homogeneous grammar of money, rising emissions and increasing extreme weather events simply do not exist. The centrality of this market-element has been rightly and aptly critiqued by the climate justice movement on several points. First, by pointing out that the CERs’ low price has spurred speculative investments rather than ecologically-sound practices, making it impossible to envisage and implement alternative ways of reducing GHGs emissions (Childs, 2012). Second, activists denounced so-called double counting, namely the simultaneous account of alleged CDM-induced emissions reductions both in the proponent state and in the hosting nation (Lohmann, 2006).[17] Finally, CDM has been dubbed as carbon colonialism in terms of its reliance on the long-standing power unevenness that defines international relations. The carbon colonialism critical argument runs as follows: after having historically over-used the atmospheric carbon dump, the global North is currently postponing its emissions reductions by outsourcing them to the global South through the CDM (Bachram, 2004).

In general terms, such arguments would seem to fully justify the decommissioning of CDM as a tool for tackling climate change. From a theoretical perspective, however, it is instructive to push the criticism farther and consider one of the four requirements for the approval of a CDM project, namely additionality.[18] Additionality can be defined as the difference between a certain course of action linked to carbon markets and a counterfactual scenario built on the hypothetical continuity of past industrial behaviours. Although apparently simple and straightforward, on closer examination, the notion of additionality shows a significant number of critical flaws, both at the technical and the conceptual level. First of all, the intricate, highly complex structure of the documentation (e.g. the Project Design Document [PDD]) used to apply to the CDM poses a serious problem: although it is supposed to perform a quality-filter function, ensuring that only viable projects receive funding, it actually excludes those applicants who lack the skills to walk the labyrinth of climate bureaucracy (most notably local communities).

There are, however, other shortcomings affecting CDM and CERs, the most crucial of which is the distinction between financial additionality and environmental additionality. The former refers to whether a given project investment would have taken place in the absence of the credit-gaining CDM provisions. In principle, for a CDM project to be approved, carbon financing must be the decisive financial factor. Nonetheless, this presupposes yet another disconnect between economic and environmental rationales: lenders, be they private or institutional, follow market rules and tend to orient themselves towards projects that are profitable on their own, even without the CDM. As a consequence, CDM traders find themselves in a paradoxical position: when facing their financial bankers, they need to emphasise the high profitability of their projects; but when discussing them with the CDM Executive Board, they need to claim that the same projects would not be financially viable without carbon funds. This is just further evidence of the instability of the contemporary climate governmentality: the carbon trading dogma finds itself constantly on the brink of potential sclerosis. By this I mean that carbon markets, in order to be offered as their own remedy, must always fail to a certain extent. Even on its own terms, carbon trading is extremely fragile, since it rests on an utterly insecure foundation.

Environmental additionality is even more problematic than its financial counterpart, and it allows us to reflect on the specific sequestration of the future enacted by the CDM. Determining environmental additionality requires: a project baseline, or reference case, that describes what would have happened in the absence of the CDM project; as set of methodologies for estimating a project’s actual GHG emissions reduction. Moreover, environmental additionality requires a quantitative comparison of actual emissions to baseline projections. The difference between the baseline and actual emissions (i.e. the volume of GHGs abated) is the amount of environmental additionality achieved by the project. In other terms, CDM environmental additionality requires the mobilization of both a calculative and a promissory apparatus that, taken together, provide a technical support to the carbon trading dogma. This support takes the form of an ideological de-politicization of decision-making (Swyngedouw, 2011). In order to create a common plane of comparability between the (hopeful) future prescribed by the CDM project and the (catastrophic) future designated by the counterfactual baseline, any radical presupposition has to be ruled out: the CDM is depicted as the only alternative to the hypothetical Business As Usual (BAU) scenario. As a corollary of this, the BAU future course of action must also be a continuum of the existing course, dependent on calculations conducted in the present. But this path dependency is a political choice: the dark future projected by planetary global warming appears to be avoidable only by the intervention of the CDM. Lohmann poignantly elaborates on this ideological articulation of market freedom and historical determinism:

For accounting to be possible and carbon credits to be saleable, each project must be framed as generating a determinate number of credits. That becomes possible only if the counterfactual scenario of the ‘baseline’ world is framed as singular, that is, separated out from a large number of other theoretically possible without-project scenarios. […] To disentangle a single baseline necessitates framing the political question of what would have happened without projects as a matter of technical prediction in a deterministic system about which near-perfect knowledge is in principle possible. Social conditionalities that do not easily lend themselves to prediction (socio-economic development, demographic trends, future land use practices, international policy making, etc.) are reduced to technical and methodological uncertainties. Project proponents, by contrast, must be framed non-deterministically, as free decision-makers, if their carbon project initiatives are to be seen as ‘making a difference’. (Lohmann, 2009: 511)

Thus, the calculative/promissory support of carbon trading dogma relies on a perverse admixture of salvation and catastrophe that resonates with what Jean-Pierre Dupuy (2002) has called ‘enlightened doomsaying’ (catastrophisme éclairé). This notion marks a curious inversion of the present-future relationship by means of which a contemporary assessed worst-case scenario is assumed to be already verified in order for its actual future verification to be avoided. Paradoxically, then, the future ends up being conceived of as simultaneously deterministically defined and caused by societies’ political decisions. As Dupuy puts it, the future is ‘counterfactually independent from the present’ (2002: 107). Such independence, however – at least with regard to carbon trading – is predicated on the putatively indisputable assumption that only the market can eventually prevent the apocalyptic consequences of climate change. Here resides the main strength of the carbon trading dogma: by enacting a regime of truth in which the market appears as the sole saviour in the face of impending ecological collapse – despite its role in bringing about global warming in the first place – political alternatives and social oppositions are rendered not only useless, but also environmentally damaging, since alternative solutions would impede or delay the market-based solution so urgently advocated. In a compelling article, Frédéric Neyrat has argued that such enlightened doomsaying is not only compatible with Foucault’s biopolitical hypothesis, but represents its contemporary configuration in the form of a biopolitique des catastrophes. Neyrat rightly points out that ‘the biopolitics of catastrophes occludes a proper eco-politics. The political management of the possible future devours it [la gestion politique du possible est la digestion du possible] and makes another politics impossible’ (2006: 115).

Conclusion

With this analysis of the historical and technical specificity of carbon commodities, we can now address the questions posed in the Introduction, of the ideal conditions of carbon markets, and whether carbon trading can actually help mitigate climate change. First, with respect to the ideal conditions under which carbon markets could be expected to work the concept of carbon trading dogma provides a suitable perspective to read the emergence and evolution of carbon markets in relation to both the fundamental tendencies of contemporary capitalist development and the material features of carbon commodities. Furthermore, we can see that the central element in the analysis of the carbon trading dogma is the discursive entrenchment of its essential equation (environmental preservation = production of surplus value/sustainable growth), that is, its ability to crystallize the will and political imagination along market lines. While internally differentiated, such crystallizations are marked by the same formal, governmental principle: economic competition. The discursive entrenchment of market solutions makes it virtually impenetrable to criticisms or to contradictory empirical evidence. This makes it difficult, perhaps even impossible, to specify any sort of ‘ideal’ conditions of carbon markets: they constantly enact a sort of productive failure which, far from being a side-effect of their deployment, could more accurately be described as their fundamental logic. Failure is their ideal condition!

The second question posed in the Introduction asked whether carbon trading could be beneficial to climate change mitigation efforts. Answering this question is more difficult, because it is so tempting to shout a resolute: ‘No!’. There is little doubt about it: carbon markets have been not only useless in fighting climate change, but also damaging. Moreover, insofar as carbon commodities conform to the carbon trading dogma, it is to be expected that the disjunction between (putative) environmental goal and (actual) monetary means will remain operative. However, if we wish to avoid throwing out the baby with the bath water, recognition of this disjunction will not be sufficient.

What do I mean by this? From the perspective of operaismo (workerism)[19] – namely the theoretical basis of this paper – struggle precedes capitalist organization. As Mario Tronti stated:

We too have worked with a concept that puts capitalist development first, and workers second. This is a mistake. And now we have to turn the problem on its head, to change perspective and start again from the beginning: and the beginning is the class struggle of the working class. (Tronti, 2006: 39)

If this is true, then both the new role of the general intellect as the organizing principle of production and the new governmental function performed by financialization have their roots in the tremendous waves of global struggles of the 1960s and 1970s. Environmental issues are no exception: without social movements that placed ecological issues on private and public agendas alike, nobody would have cared about ecology. The crucial role of social struggles also holds true for climate change and carbon markets. Thus, the carbon trading dogma is not an unassailable fortress; on the contrary, even its internal consistency shows signs of decay (not to mention all the opposition it has elicited and continues to bring forth). This is the level of abstraction at which something like a climate class struggle is taking place.[20] This is also the crucial terrain upon which political ecology and climate justice should wage their battles: framing resistance as the catalyst of political instances that cannot be reduced to a governmental rationality based solely on the market logic. Antagonism, then, would become the vehicle of translation of those instances into the institutional language of environmental policy, not only as it is currently conceived, but also as it could be envisaged after the incorporation of new political horizons. Thus, I contend that contemporary climate struggles – including the protest by hundreds of thousands across 150 countries who took part in the People’s Climate March on September 21st 2014 – are disarticulations of the carbon trading dogma which simultaneously undermine its functioning and prefigure alternative solutions to global warming. Following an intuition of Italian philosopher Carlo Sini (2012), I would like to conclude on a provocative note: what if financial (carbon) markets themselves are but the most amazing commons awaiting to be saved from themselves, from their own privatistic disease?

* This research is co-funded by the European Social Fund through the Operational Human Potential and by the National Portuguese Funds through the Foundation for Science and Technology in the context of the Post-Doctoral Grant SFRH/BPD/96008/2013; Centre for Social Studies, University of Coimbra. The author wishes to thank Stefania Barca and Nick Dyer-Witheford for their supervision and support, Adina Arvatu and Steven Sampson for linguistic advice, and the two anonymous reviewers for their valuable suggestions.

[1] It is important to stress that the very idea of carbon trading originated from the private sector. In fact, as Newell and Paterson observe: ‘Promoters of the voluntary carbon offset markets never tire of pointing out they precede the regulatory markets. The first such transaction was in 1989, when AES, a US electricity company, invested in a forestry plantation (of pine and eucalyptus) in Guatemala to offset the emissions from its new coal-fired power plant in Connecticut’ (Newell and Paterson, 2010: 109).

[2] A tonne of carbon dioxide equivalent (tCO2e) is the measurement unit of carbon in the dedicated markets.

[3] For a critical account of Durban COP 17, see Bond (2012a).

[4] For a detailed analysis of each flexibility mechanism, see Gupta (2014).

[5] For a detailed review of critiques of carbon markets, see the following compelling sources: Lohmann (2006); Böhm and Dhabi (2009); Gilbertson and Reyes (2009); Böhm, Murtola and Spoelstra (2012).

[6] The Climate Summit 2014, held in New York on September 23rd, was organized by UN Secretary General Ban Ki-moon. He invited leaders of governments, the private sector, and civil society to unite in concrete action towards a low-carbon world. The meeting was preceded by the People’s Climate March, a large-scale activist event to advocate global action against global warming. With over 400,000 participants, it was the largest climate march in history.

[7] See for example Barron (2012), Irwin (2012) and McCoy and Weise (2012).

[8] By governmental dispositif, I mean – following Foucault – the connecting space by means of which power organizes and manages a set of heterogeneous elements (which may be discourses, spatial architectures, administrative procedures, philosophical propositions, technological innovations, etc.) (Chignola, 2014).

[9] It is not only knowledge that is involved in this restructuring of capitalist production. As Maurizio Lazzarato argues: ‘We are faced with a form of capitalist accumulation that is no longer only based on the exploitation of labour in the industrial sense, but also on that of knowledge, life, health, leisure, culture etc. What organizations produce and sell not only includes material or immaterial goods, but also forms of communication, standards of socialization, perception, education, housing, transportation etc’. (2004: 205).

[10] The hypothesis of a cognitive form of capitalism has been widely discussed in the last decade. See for example Vercellone (2006); Leonardi (2010); Peters and Bulut (2011).

[11] This means that capital gains tend to replace wages in the composition of households’ income. As shown by Andrea Fumagalli and Stefano Lucarelli (2011), when the productivity of the economic system significantly depends on learning and network economies, cumulative growth occurs if and only if the sum total of capital gains-dependent investment propensity and consumption propensity is higher than the salary-dependent consumption propensity. Such dynamics can be analyzed also from the perspective of financial wealth-effects (Lucarelli and Leonardi, 2015).

[12] Weather-derivatives are designed to price and trade both in the uncertainties of the weather and social uncertainties about the future of climate change. CAT bonds are insurance-like mechanisms that are putatively intended to disperse catastrophic weather risk and, in so doing, to protect vulnerable sectors such as agriculture and coastal property. For a compelling analysis of such financial tools, see Cooper (2010).

[13] Along similar lines, Stefan C. Aykut and Amy Dahan (2015) propose the term reality schism (schisme de réalité) to indicate a twofold disconnect. First, the disconnect between policy inactivity and climate degradation. Second, the disconnect between the increasing exploitation of natural resources as fostered by global markets and the UN imaginary of powerful regulatory mechanisms that can control the crisis.

[14] This point requires a clarification. In a compelling article, Romain Felli (2014) argues that carbon credits or permits should not be considered as commodities, since no socially-necessary labour time is crystallized in them. Thus, neither European Union Allowances nor Certified Emission Reductions are elements of a new accumulation strategy. Rather, they are conceived of as public entitlements to emit greenhouse gases and, as such, are essential components of climate rent. My use of the term climate rent significantly diverges form Felli’s. The main difference is that I am convinced that (cognitive) labour – and its exploitation – is actually prominent in the production of carbon commodities. As a consequence, these latter disclose an unprecedented site of accumulation (which is governed by financial means). If this is true, then the social form of rent undergoes a significant transformation. Carlo Vercellone (2010; 2013) has named it becoming rent of profit. Rachel O’Dwyer articulates the very core of such a transformation: ‘Capitalist accumulation is today characterized by a shift from the productive forms of capitalism that characterized the industrial era towards new modalities in which rent is no longer cast in opposition to profit. Through the growing role of property in extracting value from a position external to production, and the manipulation of the social and political environment in which economic activities occur, such as the management of scarcity and the increasingly speculative nature of capital itself, the core tenets of “rent” are confused with “profit”’ (2013: 508). Thus, my argument is that climate rent is the form of value production symmetrical to the carbon trading dogma as a crucial instance of global warming governance.

[15] A powerful critique of the Cartesian dualism in green thinking is provided by Jason Moore (2015). This author also highlights how the ecological crisis needs to be read in connection with the historical transformation of capitalist processes of value-creation.

[16] It is worth noting that this geopolitical issue is the most controversial within global warming governance as a whole. “The recent COP 21 in Paris (December 2015) and COP 22 in Marrakech (November 2016) have just confirmed this.

[17] It is important to stress that double counting is not merely a technical problem susceptible to quick design-fixes; rather, it is an intrinsic risk pertaining to carbon offsets as second order abstractions. As James Kohm, associate director of enforcement at the US Federal Trade Commission’s bureau of consumer protection, has remarked: ‘Offsets are not like products that you can touch or feel. I might sell you an offset for planting a tree, but how do you know that I have not also sold that offset to someone else?’ (Kohm quoted in Schmidt, 2009: 65).

[18] The other three requirements are: the compatibility between the project and the overall goal of sustainable development of the host country; the priority of environmental dimensions over economic ones (the project must demonstrate that it was not already registered for funding in the host country’s development plan); the supplementarity of the project with regard to the investing country’s reduction strategy, meaning that the CDM cannot represent more than a small fraction of the general approach to the KP’s targets.

[19] On the heterodox stream of Western Marxism named operaismo, see Dyer-Witheford (1999); Borio, Pozzi and Roggero (2002) and Wright (2002).

[20] In a recent article, Steffen Böhm, Maria Ceci Misoczky and Sandra Moog address the issue of carbon trading by arguing that ‘even if a decarbonized capitalist “green economy” were possible, such an economy would be characterized by uneven growth and disparities of income, and by unequal distribution of economic, social and environmental risks that global markets produce’ (Böhm, Misoczky and Moog, 2012: 1621). They put forward such an argument by reviewing four Marxist approaches as articulated by John Bellamy Foster, Jason Moore, David Harvey and Rui Marini. It is my impression that these concluding remarks may embryonically gesture towards a fifth Marxist approach to carbon markets, namely a workerist one.

AAVV (2013) ‘EU ETS Myth Busting’. [http://www.tni.org/briefing/eu-ets-myth-busting]

Aykut S. and A. Dahan (2015) Gouverner le climat? 20 ans de négociations internationales. Paris: Presses de Sciences Po.

Bachram, H. (2004) ‘Climate fraud and carbon colonialism: The new trade in greenhouse gases’, Capitalism, Nature, Socialism, 15(4): 1-16.

Barrett, P. (2012) ‘It’s global warming, stupid!’, Bloomberg Businessweek, 1 November.

Barron, J. (2012) ‘After the Devastation, a Daunting Recovery’, The New York Times, 31 October. [http://www.nytimes.com/2012/10/31/us/hurricane-sandy-barrels-region-leaving-battered-path.html?pagewanted=all&_r=0]

Böhm, S. and S. Dabhi (eds.) (2009) Upsetting the offset: The political economy of carbon markets. London: MayFlyBooks.

Böhm, S., Misoczky, M-C. and S. Moog (2012) ‘Greening capitalism? A Marxist critique of carbon markets’, Organization Studies, 33(11): 1617-1638.

Böhm S., A-M. Murtola, and S. Spoelstra (eds.) (2012) ‘The atmosphere business’, ephemera 12(1-2).

Bond, P. (2012a) ‘Durban’s conference of polluters: Market failure and critic failure’, ephemera, 12(1-2): 42-69.

Bond, P. (2012b) Politics of climate justice. Durban: University of KwaZulu-Natal Press.

Bond, P. and Sharife, K. (2012) ‘Climate financing crisis and the CDM’s crash’, in P. Bond (ed.) The CDM in Africa cannot deliver the money. University of KwaZulu Natal Centre for Civil Society (SA) and Dartmouth College Climate Justice Research Project (USA) for EJOLT (Environmental Justice Organisations Liabilities and Trade. [http://climateandcapitalism.com/files/2012/04/CDM-Africa-Cannot-Deliver.pdf]

Borio, G., F. Pozzi and G. Roggero (2002) Futuro anteriore. Roma: Deriveapprodi.

Callon, M. (2009) ‘Civilizing markets: Carbon trading between in vitro and in vivo experiments’, Accounting, Organizations and Society, 34(3-4): 535-548.

Chakrabarty, D. (2009) ‘The climate of history: Four theses’, Critical Inquiry, 35(2): 197-222.

Chignola, S. (2014) ‘Sul dispositivo. Foucault, Agamben, Deleuze’, paper presented at UNISINOS, Porto Alegre, Brazil, September 25.

Childs, M. (2012) ‘Privatizing the atmosphere: A solution or a dangerous con?’, ephemera, 12(1-2): 12-18.

Cooper, M. (2010) ‘Turbulent worlds: Financial markets and environmental crisis’, Theory, Culture and Society, 27(2-3): 167-190.

Dardot, P. and C. Laval (2014) The new way of the world. London: Verso.

Descheneau, P. and M. Paterson (2011) ‘Between desire and routine: Assembling environment and finance in carbon markets’, Antipode, 43(3): 662-681.

Dupuy, J-P. (2002) Pour un catastrophisme éclairé. Paris: Seuil.

Dyer-Witeford, N. (1999) Cyber-Marx. Champaign, IL.: University of Illinois Press.

Edwards, P. (2010) A vast machine. Cambridge: Cambridge MA, MIT Press.

Felli, R. (2014) ‘On the climate rent’, Historical Materialism, 22(3-4): 251-280.

Foucault, M. (2007) Security, territory, population. New York: Palgrave Macmillan.

Foucault, M. (2008) Birth of biopolitics. New York: Palgrave Macmillan.

Fletcher, R. (2012) ‘Capitalizing on chaos: Climate change and disaster capitalism’, ephemera, 12(1-2): 97-112.

Fumagalli, A. and S. Lucarelli (2011) ‘A financialized monetary economy of production’, International Journal of Political Economy, 40(1): 48-69.

Gilbertson, T. and O. Reyes (2009) Carbon trading: How it works and why it fails. Uppsala: Dag Hammarskjöld Foundation.

Gupta, S. et al. (2007) ‘Policies, instruments, and co-operative arrangements’, IPCC, Climate Change 2007: Mitigation. Cambridge: Cambridge University Press.

Gupta, J. (2014) The history of global climate governance. Cambridge: Cambridge University Press.

Iacomelli, A. (2005) Oltre Kyoto. Rome: Franco Muzzio Editore.

Irwin, N. (2012) ‘What Hurricane Sandy means for the economy’, The Washington Post, 30 October. [https://www.washingtonpost.com/business/economy/what-hurricane-sandy-means-for-the-economy/2012/10/30/e6ef95ea-2293-11e2-8448-81b1ce7d6978_s...

Klein, N. (2014) This changes everything. London: Allen Lane.

Lazzarato, M. (2004) ‘From capital-labour to capital-life’, ephemera, 4(3): 187-208.

Leonardi, E. (2010) ‘The imprimatur of capital: Gilbert Simondon and the hypothesis of cognitive capitalism’, ephemera, 10(3-4): 253-266.

Leonardi, E. (2012) Biopolitics of climate change: Carbon commodities, environmental profanations, and the lost innocence of use-value. University of Western Ontario. [doctoral dissertation; http://ir.lib.uwo.ca/etd/959/]

Lohmann, L. (2006) Carbon trading: A critical conversation on climate change, privatization, and power. Uppsala: Dag Hammarskjöld Foundation.

Lohmann, L. (2009) ‘Toward a different debate in environmental accounting: The cases of carbon and cost-benefit’, Accounting, Organizations and Society, 34: 499-534.

Lohmann, L. (2011a) ‘Regulation as corruption in the carbon offset markets.’ In T. Reddy (eds.), Carbon trading in Africa: A critical review. Pretoria: Institute for Security Studies.

Lohmann, L. (2011b) ‘Financialization, commodification, and carbon: The contradictions of neoliberal climate policy’, in L. Panitch, G. Albo and C. Vivek (eds.) Socialist register 2012: The crisis and the left. New York: Monthly Review Press.

Lohmann, L. (2011c) ‘The endless algebra of carbon markets’, in P. Bond (ed.) Durban’s climate gamble: Trading carbon, betting the earth. Braamfontein: University of South Africa Press.

Lucarelli, S. (2010) ‘Financialization as biopower’, in A. Fumagalli and S. Mezzadra (eds.) Crisis in the global economy. Los Angeles: Semiotext(e).

Lucarelli, S. and C. Vercellone (2013) ‘The thesis of cognitive capitalism. New research perspectives: An introduction’, Knowledge Cultures, 1(4): 2-14.

Lucarelli, S. and E. Leonardi (2015) ‘Financial governmentality: The wealth-effect as a practice of social control’, in M. Peters, J. Paraskeva and T. Besley (eds.) The global financial crisis and educational restructuring. Bern: Peter Lang AG.

McCoy, K. and E. Weise (2012) ‘Sandy leaves millions without power; 16 dead’, USA Today, 29 October. [http://www.usatoday.com/story/weather/2012/10/29/hurricane-sandy-east-coast-frankenstorm/1666105]

Marazzi, C. (2011) The violence of financial capital. Los Angeles: Semiotext(e).

Marcu, A. (2016) ‘Carbon Market Provisions in the Paris Agreement (Article 6): Avoiding the trap of carbon metrics’, CEPS Special Report, 128 [http://www.ceps-ech.eu/sites/default/files/SR%20No%20128%20ACM%20Post%20COP21%20Analysis%20of%20Article%206.pdf]

Marx, K. (1990) Capital: Volume I. New York: Vintage Books.

Marx, K. (1993) Grundrisse: Foundations of the critique of political economy. London and- New York: Penguin Books.

Moore, J. (2015) Capitalism in the web of life. London: Verso.

Moreno, C., L. Fuchs and D. Speich Chassé (2016) ‘Beyond Paris: Avoiding the trap of carbon metrics’, in Open Democracy. [https://www.opendemocracy.net/transformation/camila-moreno-lili-fuhr-daniel-speich-chass/beyond-paris-avoiding-trap-of-carbon-metr]

Newell, P. and M. Paterson (2010) Climate capitalism. Cambridge: Cambridge University Press.

Neyrat, F. (2006) ‘Biopolitique des catastrophes’, Multitude, 24(1): 107-117.

O’Dwyer, R. (2013) ‘Spectre of the commons: Spectrum regulation in the communism of capital’, ephemera, 13(3): 497-526.

Oreskes, N. and E.M. Conway (2010) Merchants of doubt. London: Bloomsbury Press.

Peters, M. and E. Bulut (eds.) (2011) Cognitive capitalism, education, and digital labour. Bern: Peter Lang AG.

Reyes, O. (2011) EU emissions trading system: Failing at the third attempt. Carbon Trade Watch. [http://www.carbontradewatch.org/downloads/publications/ETS_briefing_april2011.pdf.]

Schmidt, C. (2009) ‘Carbon offsets: Growing pains in a growing market’, Environmental Health Perspectives, 117(2): 62-68.

Sini, C. (2012) ‘La vita catturata dentro un segno’, Il Manifesto, 14 September.

Swyngedouw, E. (2011) ‘Depoliticized environments: The end of nature, climate change and the post-political condition’, Royal Institute of Philosophy Supplement, 69: 253-274.

Tronti, M. (2006) Operai e capitale. Roma: Deriveapprodi.

Vaughan, A. and K. Mathiesen (2014) ‘Ban Ki-moon opens the summit’, The Guardian, 23 September.

Vercellone, C. (ed.) (2006) Capitalismo cognitivo. Roma: Manifestolibri.

Vercellone, C. (2010) ‘The crisis of the law of value and the becoming rent of profit’, in A. Fumagalli and S. Mezzadra (eds.), Crisis in the global economy. Los Angeles: Semiotext(e).

Vercellone, C. (2013) ‘The becoming rent of profit? The new articulation of wage, rent and profit’, Knowledge Cultures, 1(2): 194-207.

Virno, P. (2004) A grammar of the multitude. Los Angeles: Semiotext(e).

Whitington, J. (2012) ‘The prey of uncertainty: Climate change as an opportunity’, ephemera, 12(1-2): 113-137.

World Bank (2007) State and trends in the carbon market 2007. Washington DC: The World Bank.

World Bank (2008) State and trends in the carbon market 2008. Washington DC: The World Bank.

World Bank (2009) State and trends in the carbon market 2009. Washington DC: The World Bank.

World Bank (2010a) State and trends in the cCarbon market 2010. Washington DC: The World Bank.

World Bank (2010b) World development report 2010: Development and climate change. Washington DC: The World Bank.

World Bank (2011) State and trends in the carbon market 2011. Washington DC: The World Bank.

World Bank (2012) State and trends in the carbon market 2012. Washington DC: The World Bank.

World Bank (2014) State and trends of carbon pricing 2014. Washington DC: The World Bank.

Wright, S. (2002) Storming heaven. London: Pluto Press.